FOR IMMEDIATE RELEASE:

April 19, 2019

Contact: Paige Kelly, pkelly@socialsecurityworks.org

Democrats have concrete plans to restore Social Security to long-range actuarial balance and expand benefits

Washington, D.C. – As reporters prepare to cover the soon-to-be-released 2019 Social Security and Medicare Trustees Reports, Social Security Works provides you with this background analysis, which summarizes what are likely to be the Social Security Report’s key findings (based on last year’s forecasts), and puts them in context. Please note that this backgrounder addresses only the Social Security cash benefits Trustees Report (Old Age, Survivors, and Disability Insurance Trustees Report), and not the Medicare Trustees Report.

In addition to reviewing this backgrounder, we invite you to speak with our president, Nancy Altman, who is a nationally recognized Social Security expert. (See her bio below.) We also urge you to review our fact sheet that discusses, among other things, misinterpretations by non-experts caused by over-emphasis of unrealistically long valuation periods.

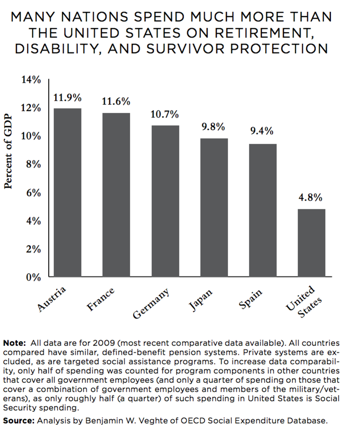

The most important takeaways from the 2019 Trustees Report will be that (1) Social Security has a large accumulated surplus, and (2) Social Security is extremely affordable. In three-quarters of a century, in 2095, Social Security will constitute just around 6.16 percent of GDP. That is considerably lower, as a percentage of GDP, than Germany, Austria, France, and most other industrialized countries spend on their counterpart programs today.

{kind=link}

The 2019 Trustees Report will project Social Security’s cumulative surplus to be roughly $2.9 trillion. It will show that Social Security is fully funded until around 2034, around 93 percent funded for the next 25 years, around 87 percent funded over the next 50 years, and around 84 percent funded over the next 75 years.

(Those percentages are calculated from the 2018 report. This year’s report may vary slightly, but not significantly. As soon as the report is released, this backgrounder will be updated with the latest projections and released as a fact sheet.)

Often, the release of the annual Trustees Report leads to lamentations from many observers that “Congress has no plan to address Social Security’s projected shortfall.” That is incorrect. It is only Congressional Republicans who have no plans – at least that they are willing to publicly embrace. That is perhaps because their preferred “solutions” involve benefit cuts, which are overwhelmingly opposed by voters across the political spectrum, including their own Republican base.

In contrast, Congressional Democrats have concrete plans – not just to ensure that all promised benefits will be paid in full and on time for the foreseeable future, but to address our nation’s retirement income crisis by increasing Social Security’s modest benefits. The Social Security 2100 Act, introduced by Rep. John Larson (D-CT), has over 200 cosponsors in the House of Representatives. Larson has held several hearings on the bill and intends to bring it to the House floor this spring.

Several other bills to protect and expand Social Security benefits have been introduced in the House and Senate, and nearly every 2020 presidential candidate serving in Congress is a member of the bicameral Expand Social Security Caucus.

The question of whether to expand or cut Social Security’s modest benefits is a question of values and choice, not affordability. Indeed, in light of Social Security’s near universality, efficiency, fairness in its benefit distribution, portability from job to job, and security, the obvious solution to the nation’s looming retirement income crisis is to increase Social Security’s modest benefits. The average annual benefit received by Social Security’s over 63 million beneficiaries is only about $16,000 this year.

Over half (52 percent) of American households headed by someone of working age will not be able to maintain their standards of living in old age. This figure rises to roughly two-thirds when health and long-term care costs are also considered. Traditional employer-sponsored defined benefit pension plans are disappearing, leaving workers, at best, 401(k) and other retirement savings plans, which have proven inadequate. Around half of households aged 55 or older had zero retirement savings in 2013. Among those households age 55-64 with some retirement savings in 2013, the median amount of those savings was about $104,000, equivalent to an annuity of just $310 a month. Thus, it is not surprising that today two-thirds of senior beneficiaries rely on Social Security for a majority of their income. Social Security will certainly be even more important to tomorrow’s seniors.

Expanding Social Security not only addresses the retirement income crisis, it also is part of the answer to growing income and wealth inequality and the financial squeeze on working families. Expanding, not cutting, Social Security while requiring the wealthiest among us to contribute more – indeed, their fair share – is the best policy approach to addressing these challenges while restoring Social Security to long-range actuarial balance. Cutting those modest benefits will only exacerbate these challenges.

__________________

Nancy Altman, President of Social Security Works and Chair of the Strengthen Social Security Coalition, has a 40-year background in the areas of Social Security and private pensions. She has taught at Harvard University. She served as Alan Greenspan’s assistant in his position as chairman of the so-called Greenspan commission, the bipartisan commission whose recommendations formed the basis of the Social Security Amendments of 1983. She is the author of The Truth About Social Security (Strong Arm Press, 2018), The Battle for Social Security: From FDR’s Vision to Bush’s Gamble (John Wiley & Sons, 2005), and co-author, with Eric R. Kingson, of Social Security Works! Why Social Security Isn’t Going Broke and How Expanding It Will Help Us All (The New Press, 2015).

For more information about Social Security Works or the Strengthen Social Security Coalition, visit http://socialsecurityworks.org/.